With diversification at its heart, the Swiss pension scheme embraces best practices deriving from the oft-quoted concept of ‘not putting all your eggs in one basket‘.

What is the Swiss pension scheme?

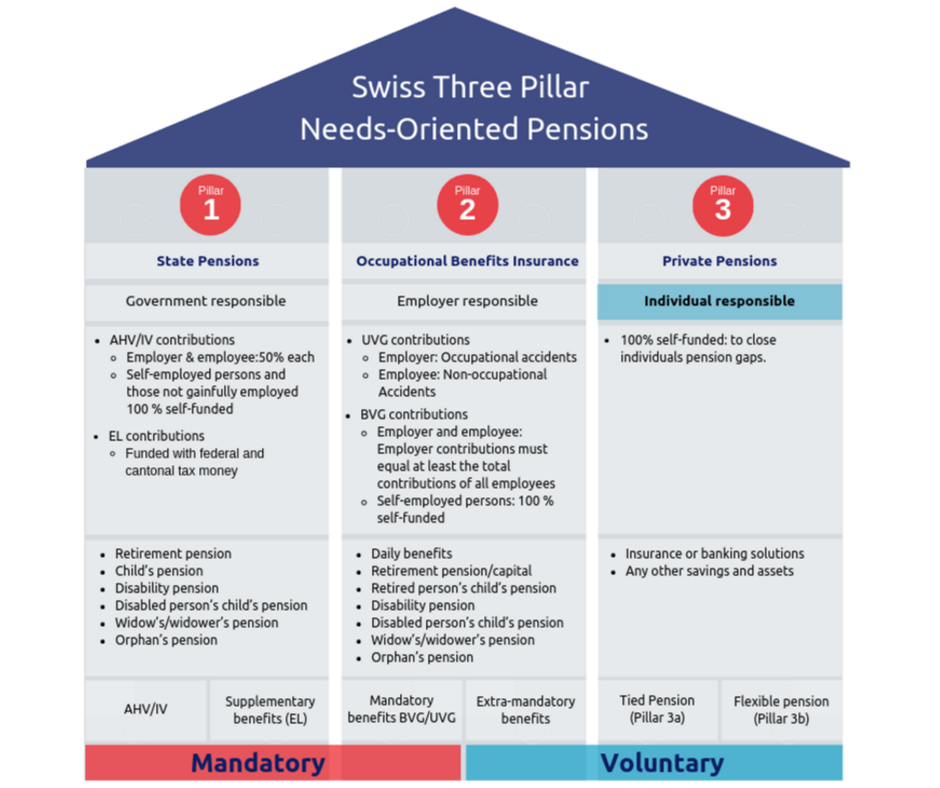

In a nutshell, the Swiss pensions system is a multifaceted system consisting of three pillars:

Pillar 1: The Swiss State Pension

Mandatory and meant to provide individual and survivors pensions to cover basic needs following retirement.

Pillar 2: Occupational Pensions

Pillar 2 is compulsory for all employed individuals and intended to provide a ‘comfortable’ income after retirement. Occupational pensions are funded by employer and employee contributions for employed individuals, and voluntarily self-funded by self-employed individuals.

Pillar 3: Optional Pensions

Swiss Pillar 3a & Pillar 3b pensions are voluntary and designed to augment Pillar 1 and 2 pensions aimed to maintain the lifestyle you want post-retirement. These pensions are funded by an individual’s voluntary contributions. There are two types of Swiss Pillar 3 pensions:

- Swiss Pillar 3a: Tied pensions. Long-term plans. Capital locked into the retirement plan. Annual contributions are restricted, and the yearly maximums differ depending on whether you have a Pillar 2 occupational benefits plan or not. You can find the current Pillar 3a maximums here.

- Swiss Pillar 3b: Flexible pension plans. No statutorily prescribed term. Capital available at any time. No financing restrictions.

How does the Swiss pension system work?

Switzerland’s statutory framework provides 3 pillars that support the security of every person and their dependents within the Swiss pension system.

Pillar 1 is the mandatory state pensions for which the Swiss Government is responsible.

Pillar 2 represents compulsory occupational benefits insurance, including retirement pensions and capital, for which the employer is responsible if you are employed, and is your responsibility if you are self-employed.

Pillar 3 is where individually tailored, flexible private pensions live. These schemes are voluntary and designed to help you maintain your living standards following retirement. Tied Pillar 3a pensions are long-term plans where capital is locked into a retirement plan. Flexible Pillar 3b pensions are plans that do not have a prescribed term, where the capital is available at any time.

Given that Pillar 1 pensions are mandatory, and Pillar 2 compulsory for employed persons, Pillar 3 is where you get the chance to make lifestyle decisions about funding your time after retirement.

What are the main differences between Swiss Pillar 3a and 3b contributions?

When it comes to financing a Pillar 3b pension, no restrictions apply. However, with a Pillar 3a pension, Swiss law restricts the maximum annual contribution you can make.

The contribution you can pay into your Pillar 3a depends on whether you have a Pillar 2 occupational pension or not, which largely depends on whether you are employed or self-employed. You can find the current maximum amounts here.

The tax aspects of investing in a Pillar 3a pension are particularly interesting. Currently, payments are tax-deductible up to an annual tax advantage of CHF2,000. Money available at maturity is not taxed as regular income, but at a special rate, which the Swiss government generally reviews and adjusts every two years.

One of the critical differences between Pillar 3a and Pillar 3b is that the capital tied up in a Pillar 3a pension is not available to you until maturity whereas, capital invested in a Pillar 3b scheme is available to you at any time.

3a for tax advantages, 3b for flexibility

Pillar 3b pensions are all about flexibility while providing an efficient financial vehicle to help you live the life you want when you retire.

Pillar 3a:

- Tied pensions

- Long-term plans

- Annual contributions restricted

- Capital locked into the retirement plan

Pillar 3b:

- Flexible pension plans

- No statutorily prescribed term

- No financing restrictions

- Capital available at any time

What is the best Pillar 3 strategy?

When it comes to the mechanics of investing in Pillar 3 pensions, funding Pillar 3a to the maximum each year should be the priority as this will help you optimise both your retirement provision and your tax bill. You can find out what the current annual maximum statutory Pillar 3a contribution is here.

Once you have maximised your Pillar 3a contributions, you’ll want to make sure you have enough in your 3b fund for your future lifestyle. To make sure your life in later years is all you want it to be, you should seriously consider taking full advantage of the Pillar 3b opportunities available to you. Lifestyle Financial Planning can help you work out exactly how much money you will need to fund your future retirement lifestyle.

What are the advantages of contributing to your Swiss Pillar three pension?

Tax relief

This is the most widely known advantage of contributing to both Pillar 2 and 3 pensions. Payments made to Pillar 3a plans are tax-deductible, and payment at maturity is taxed at a reduced rate. Reduce your annual tax bill by paying the maximum into a Pillar 3 pension.

It’s personal

Pillar 3b provides an opportunity to craft an optimum investment strategy forged around your needs, goals, attitude to risk, investment time frame, and security requirements.

Maintaining the lifestyle you want

For many, Pillar 1 and 2 pensions won’t provide enough income during retirement to support their envisaged lifestyle. A Pillar 3b solution helps bridge that gap by tailoring a solution that ensures you can afford the lifestyle you want to lead when you retire.

Investment diversification

Pillar 3b pensions allow you to diversify your investment; optimising returns, liquidity, capital protection, and coverage for risk.

Flexibility

Many people think that a signed pension policy can’t be changed until the end of the contract. Many pillar 3b plans can, however, be changed and adapted as your circumstances evolve without any significant disadvantage. So, your pension plan grows with you, for you.

Risk reduction and maximising return

Pensions and investment products have evolved over recent years,. Those available within Pillar 3b options now enrich the investment experience by offering innovative concepts for minimising risk and enhancing returns.

Most include:

- Dynamic capital accumulation with higher return targets

- Investment profiles for any investment strategy

- Planned disbursement

- Capital availability

- Options for a lump sum death payment or occupational disability pension

Security and peace of mind

Pillar 3b insurance solutions offer advantages like guaranteed capital at maturity, occupational disability protection, protection for your loved ones if you should die and payment protection.

There are a considerable variety of insurance products that combine protection with capital growth. These can be adapted to suit any lifestyle and designed to focus on your future.

What are common Swiss Pillar 3b misunderstandings?

Expats and Swiss nationals alike, often select the Pillar 3b solution offered by their bank. For some, this is the right solution, but many choose this pillar 3b option without realising there are other options available.

Taking the time to reflect on your financial goals will help you pick the best solution for you and your family.

Why choose a banking solution?

If you have no-one you need to protect financially, like a partner or children, a banking solution may be right for you.

Contributions are entirely voluntary and not tied to defined times and amounts, so a banking solution may suit you if you don’t want the structure a savings plan brings.

As there are no contract terms, no payment obligations, and it’s possible to change banks when you want, the key incentive for adopting an unstructured banking solution is flexibility.

Why choose an insurance solution?

Alongside guaranteed capital on maturity, insurance solutions offer occupational disability protection, protection for your loved ones if you should die and payment protection.

In short, while Pillar 3b insurance solutions also offer a great deal of flexibility, their byword is ‘security’.

Insurance products combine protection with capital growth. There are a wide variety of insurance products that can be adapted to suit any lifestyle and designed to focus on your future.

What are the next steps for your 3b contributions?

Researching the many pillar 3b options available can be a time-consuming and confusing undertaking. Broadly, however, as discussed earlier, these fall into two categories; solutions offered by banks, and those provided by insurance companies.

When deciding what the best Pillar 3b solution is for you, your circumstances and what you want to achieve in the future are the most important things to consider.

No-one knows for sure what might happen in the future. So, it makes a great deal of sense to identify private pensions that resonate with your financial goals and individual circumstances.

Whether you want the flexibility offered by a banking solution or the security provided by an insurance solution, your decision should always be based on your circumstances both now and in the future. Properly analysing where you are now, determining where you want to be in the future, and planning how to get there is no mean feat.

Before choosing the right option for you, it is essential you seek advice from an adviser who entirely focuses on you, your family, and your goals. This should be someone who can fully understand your current circumstances and your future desired lifestyle and can help you design a path between the two.