President Trump also led his first official trip abroad and, despite mixed media coverage, a few gaffs, and that FBI investigation, the US market remained optimistic, contrary to original predictions. The question of how long market optimism will continue in the face of on-going mixed economic performance remains to be seen.

The cheap valuation of Japanese equities has fuelled more foreign buying in May despite a currency rise. The Eurozone also continues to show positive economic data, in part bolstered by the Macron victory. As the French take to the voting booths again this week, we wait to see whether Macron can deliver a majority government.

The UK in brief

- Top performance of large cap stocks

- FTSE 100 gained 4.4%

- Mid-cap stocks gained 1.8%

- Smaller companies gained 2.3%

- Barrel prices dropped back below $50

- 8% sector loss for oil and ranking at the bottom of the table

- Top performance for Vodafone driving mobile telecoms to top of table

Food costs continue to rise, slowing spending. Uncertainty around government and policy is unlikely to bolster household spending in coming months, with all signs pointing towards higher inflation in the UK.

Commentators noted that, after an extended period of undershooting the 2% target inflation level, the Bank of England has scope to let inflation run above target for a while to “inflate away” some of the considerable debt the economy now carries.

Europe in brief

- Equities advanced at start of month

- Strong performance from Dax (++1.42%) and Spanish IBEX (+1.53%)

- CAC 40 lost initial lead closing at +0.31%

- Hedge funds are now net long the Euro

- Euro gained 3.18% against the Dollar and 3.65% against Sterling

- UK political result likely to impact further on Euro performance

- Manufacturing sector healthy

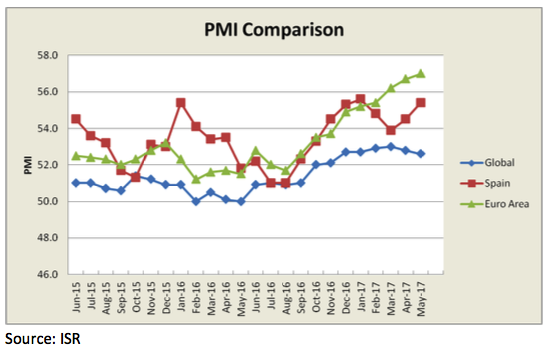

- Spanish manufacturing jobs hit 19 year high

Inflation was the lowest since December, as energy and services prices rose at a slower pace; this supports comments made by the President of the ECB, Mario Draghi, about inflation remaining subdued and maintaining the QE stimulus programme throughout 2017.

The US in brief

- Trump withdraws from the Paris Accord

- US businesses concerned with retaliatory tariffs on American goods

- Stock value of renewable power companies fell between 5-10%

- Announcement of a $100bn arms deal with Saudi Arabia

- Defence stocks rallied after announcement

- Industrial production beats market expectations

- Unemployment figures remain at cycle low

- If Fed shrinks balance sheet by selling securities, there may be pressure on interest rates

- Home Entertainment Software and Computers & Electronics both gain 15%

- Amazon approaches $1000 a share

- AAA-rated corporate bonds rose 1.6%

While some key economic measures remain positive in the US, markets remain cautious about Trump and the long-term impact of his policies. The decision to withdraw from the Paris Accord has seen a significant divide between large tech companies such as Facebook and Apple, and Trump’s vision for America. As unemployment levels continue to fall, many wait for average earnings growth to happen.

Government bonds changed little in May although there has been a mild flattening of the curve, presenting a problem for lenders who borrow short and sell long. Higher quality AAA-rated corporate bonds rose 1.6%, outperforming the wider corporate market and high-yield bonds.

Asia in brief

- Equity markets +2.4%

- Mild strengthening of Yen against the Dollar

- Japanese tempting as P/E ratio 15.4 versus 21.7 for MSCI World Index

- Retail sales and job data above expectations

- Yield curve now consistent with their monetary policy guidelines

- Monetary easing required to achieve Bank of Japan’s inflation target

- PWC highlight $US500bn spending on Chinese core infrastructure projects

- Direct investment in “Belt and Road” projects challenging for investors

- “Belt and Road” likely to stimulate commodity prices

- New freight route from Yiwu to London reduces travel time by 50%

- Chinese credit rating downgraded by Moody’s from A1 to Aa3

The “Belt and Road” initiative holds great promise for Chinese economic performance and should have a positive impact on the rest of Asia. Sizeable investment in the project will stimulate traditional infrastructure, telecommunications and energy. The Shanghai Stock Exchange Infrastructure has already risen by 30% over the past year. This project holds great potential for China and Asia, however, for the project to be a success, there must be high-quality investments with no routes back to bad loans in Chinese Government-linked entities.

If you want to read the full market commentary provided by our partners you can do so by clicking here