As expected, he withdrew the US from the Trans-Pacific Partnership (TPP) and ordered a renegotiation of the North America Free Trade Agreement.

Trump also implemented an immediate travel ban on nationals from seven majority-Muslim countries, as well as finding time to hold Theresa May’s hand.

The markets are, however, still awaiting details of core policies likely to impact performance, like tax reforms.

With the triggering of Article 50 fast approaching, and many European countries holding key elections, the markets are in for an interesting six months.

The Netherlands, Germany, and France will all be voting in new governments in the first half of the year, and this is likely to impact markets and exchange rates.

Given that so few political and market predictions were accurate in 2016, it’s best to avoid knee-jerk reactions or to try and anticipate market responses.

Source: Bloomberg

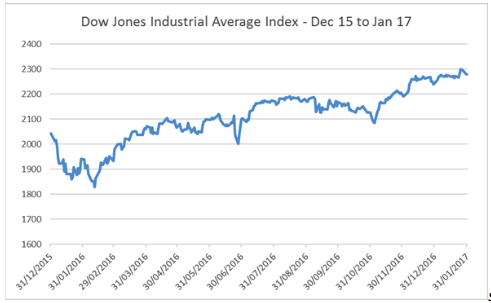

Overall market performance was positive at the start of the year. The FTSE 100 Index reached new highs mid-January after a record-breaking fourteen consecutive days of increases. European and Japanese equity indices were relatively flat, and bond markets were also range-bound.

The dollar gave up some of its recent gains, particularly against the Euro, Yen and Renminbi, having the worst January performance in over thirty years.

Trumps new administration accused Germany, Japan, and China as being currency manipulators. These kind of comments from Trump and his advisers are becoming fairly typical, and we expect them to continue into 2017.

To read more about the markets included in our Market Summary, please download the Full Market Review January 2017

.

.