UK

Brexit negotiations continue, although they don’t appear to be advancing, this leaves a veil of uncertainty hanging over the UK.

- Inflation remains at 2.6%

- Wage growth is stuck at 2.1%

- British consumer spend continues to erode

- Consumer Sentiment Index at a low of -10

- Businesses are more optimistic with their index ranking +5

- Weakened pound continues to drive profits with overseas operations

- Industrial production has trended upwards

- FTSE 100 Index recorded a gain of just 0.8%

- Provident Financial, the FTSE 100 doorstep lender, saw its shares fall by a further 57% over the month

- Conventional gilts returning +1.9% overall and up to +3.4% at the longer end

- Mark Carney suggesting that a rise in the base rate is unlikely this year

Source: Bloomberg

Europe

The main political event in Europe is the upcoming German elections. Currently, signs point to a comfortable win for Angela Merkel, who is polling ahead of Martin Schultz, the SDP leader. There is a possibility that the CDU may end up in coalition with one or more of the other parties, but the expectation overall is for no change. However, if recent elections have shown anything, it is that there are no guarantees when it comes to voter behaviour on the day.

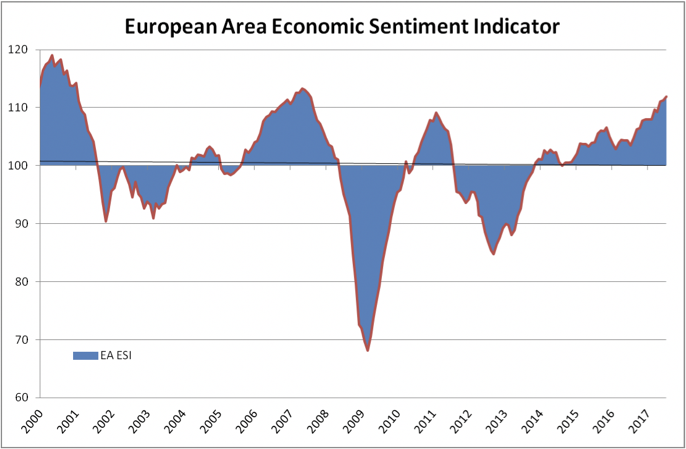

In terms of economic performance, Europe remained robust. The biggest laggard was Spanish equities, where the IBEX was down 1.93%. This was due, in large measure, to the terrorist attacks in Barcelona and Cambrils. Regarding business conditions, the manufacturing PMI index rose to 57.4 in August from 56.6 in July. This suggests ongoing growth, boosted by domestic demand and rising export orders.

- Euro Stoxx 600 Index down 0.45%

- Eurozone GDP growth came in at +0.6%

- Growth came from Spain, Netherlands and Austria

- France remained unchanged, and Germany slowed in GDP growth

- Manufacturing PMI index rose to 57.4 in August from 56.6

- Services PMI continued to slow due

- Higher than expected inflation at 1.5% from 1.3%

- Top performing sectors in the equity markets were transportation, utilities and mining

- Retail sales reported in July saw a month-on-month fall of 0.3%.

- Fixed income markets remained buoyant with sovereign bonds returning +0.8%

- Investment-grade corporate bonds returned +0.6%

Source: ISR/Eurostat

US

The majority of media attention in August centred around North Korea. Similar to Brexit predictions, many thought that this negative political atmosphere would impact markets, but over August this was not the case. President Trump’s handling of the North Korean crisis has been criticised for his attempts to use economic measures to exert influence on other Asian nations, particularly China, threatening to cut off trade with any country that does business with North Korea. Mr Trump’s determination to link the two is a departure from historical policy. It remains unclear how the US could benefit from this approach given that more than 25% of US exports go to Asia.

However, predictions remain negative; a recent Bank of America survey suggested that only 33% of money managers expect corporate profits, compared with a figure of 58% in the same survey at the start of 2017. We have seen in recent weeks how the broadly-based market uptrend has been accompanied by savage markdowns for companies that disappoint even slightly in their earnings. The survey also saw a record 46% of managers expressing the view that equity markets are overvalued, although positioning among US managers still seems to be pro-risk.

- Economic data points to a continuing recovery in the US

- The S&P 500 Index rose by 0.1%

- The Dow Jones Small Cap Index fell by 1.1%

- O’Reilly Automotive fell by 20% on announcing sales growth of just 1.7%

- Priceline had its shares marked down by 8% after it reported lower than expected second-quarter gross bookings ($20.8bn)

- The S&P 500 Index is still trading around 23% above the ten-year average.

- Industrial production pushed further with a year-on-year increase of 2.2%

- Retail sales data saw a short-term rally in the Dollar

- Over the month the US currency weakened against both the Yen and the Euro

- Fixed income stocks all offered positive returns over the month

- Long-dated conventional Treasury bonds gained 3.4%

- Index-linked stocks rose by 3.3%

Source: CIA World Factbook

Asia Pacific and Emerging Markets

In Japan ‘Abenomics’ seems to be yielding results. Prime Minister Abe appeared to recover from a series of scandals over the past few months that called into question the stability of the Abe Government. A cabinet reshuffle in late July brought in a new team of ministers and, since then, Abe’s approval ratings have improved.

South Korea has suffered from the tensions between President Trump and North Korea. The KOSPI fell 2%.

- Japanese equities were flat in August

- Led by Mitsubishi UFJ Financial (down 4.9%) the Japanese financial sector fell 3.9%

- Keyence Corporation, one of Japan’s largest technology companies, showed strong returns of 12.2%

- Japanese GDP showed the strongest result in two years rising 1.0% (quarter on quarter)

- Emerging market equities were positive returning 2.1% in local currency terms

- Emerging market equities continued to experience positive inflows

- August brought broader market participation from the financial sector led by ICBC, the world’s largest bank by assets

- China Construction Bank rose by 3.7%

- Larger capitalisation companies slightly outpaced smaller and mid-size companies

- Russia and Brazil were the standout performers with the MICEX (Russia) and BOVESPA (Brazil) indices returning 4.8% and 7.5%

- South Korea was the laggard with the KOSPI falling 2% in Won terms