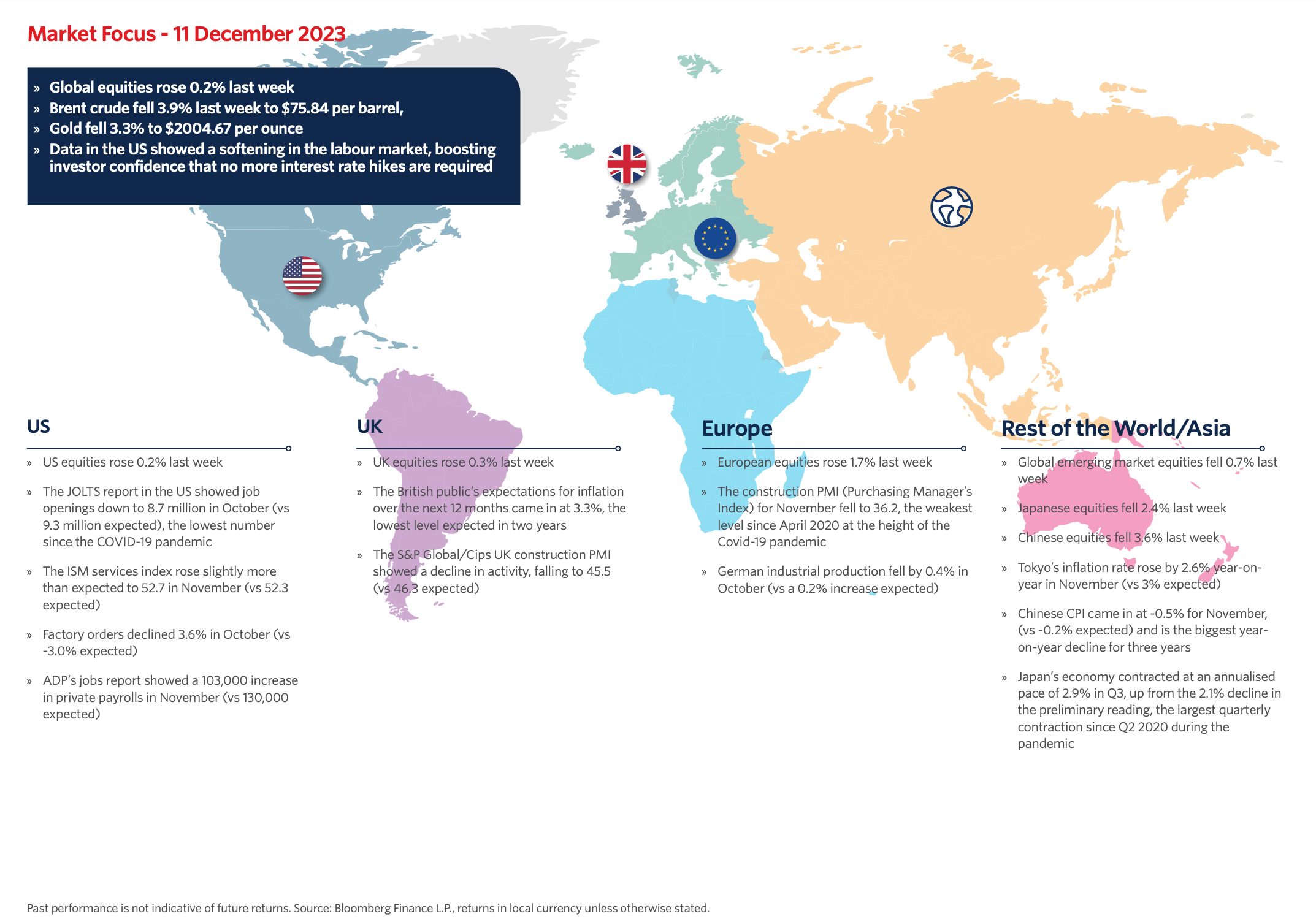

In a week marked by dynamic shifts, global equities experienced a modest uptick of 0.2%, providing a nuanced backdrop to diverse economic indicators worldwide. Here’s a snapshot of key developments across major regions:

US & UK:

- US equities edged up by 0.2%, buoyed by softer labor market data, fueling optimism that further interest rate hikes might be unnecessary.

- The US JOLTS report revealed a decline in job openings to 8.7 million in October, the lowest since the COVID-19 pandemic.

- UK equities saw a 0.3% increase, contrasting with the British public’s tempered inflation expectations of 3.3% over the next 12 months, the lowest in two years.

- S&P Global/Cips UK construction PMI dipped to 45.5, signaling a contraction in activity.

Europe:

- European equities rose by 1.7%, showcasing resilience despite challenges. However, the construction PMI for November tumbled to 36.2, the weakest level since April 2020.

- German industrial production faced headwinds, falling by 0.4% in October against an expected increase of 0.2%.

Rest of the World/Asia:

- Global emerging market equities experienced a 0.7% decline, while Japanese equities and Chinese equities saw drops of 2.4% and 3.6%, respectively.

- Tokyo’s inflation rate rose by 2.6% YoY in November, slightly below the 3% expected, while Chinese CPI registered a -0.5% decline, marking the most significant YoY drop in three years.

- Japan’s economy contracted at an annualized pace of 2.9% in Q3, the largest quarterly contraction since Q2 2020.

Commodities:

- Brent crude fell 3.9% to $75.84 per barrel, and gold experienced a 3.3% decline, resting at $2004.67 per ounce.

US Economic Indicators:

- The ISM services index rose to 52.7 in November, slightly exceeding expectations, while factory orders declined by 3.6% in October against an expected -3.0%.

- ADP’s jobs report revealed a 103,000 increase in private payrolls in November, below the anticipated 130,000.

Conclusion:

Against a backdrop of nuanced economic indicators, global equities showed resilience, with shifts in labor markets and inflation expectations influencing investor sentiment. The week’s mixed performance highlights the complex dynamics influencing markets worldwide.

Disclaimer: Past performance is not indicative of future returns. Source: Bloomberg Finance L.P., returns in local currency unless otherwise stated.

This communication is for informational purposes only and is not intended to constitute, and should not be construed as, investment advice, investment recommendations or investment research. You should seek advice from a professional adviser before embarking on any financial planning activity.