As equity markets globally surged last year and continued their positive trajectory into this year with a notable 8% increase in global equities in USD terms, it’s evident that we could be witnessing the dawn of a new bull market cycle. However, despite the promising signs, why do so few seem willing to acknowledge this?

This hesitancy could stem from a lingering psychological aftermath of recent turbulent events, such as the pandemic and subsequent inflation concerns. Investors may find themselves paradoxically attached to the negativity bred by these crises, hindering their ability to recognise or embrace the emerging positivity in the market.

The prolonged exposure to market volatility, coupled with catastrophic economic forecasts and the tangible impacts of the pandemic and inflation, has created a sense of cognitive dissonance among investors. While signs of a robust recovery are evident, such as strong corporate earnings, increased consumer spending, and improved employment rates, investors may still be hesitant to shift their mindset from one of caution to optimism. The media’s persistent focus on risks and uncertainties further reinforces this reluctance, keeping the trauma of recent market downturns fresh in investors’ minds.

Kenley Scott, Director and Global Sector Strategist at William O’Neil +, suggests that despite our observation of a downtrend, it should be perceived as a prime buying opportunity. In comparison to its predecessors, this bull market trails significantly in both duration and overall return. Drawing on historical data, we anticipate investors can anticipate notably greater returns before the conclusion of this bull market.

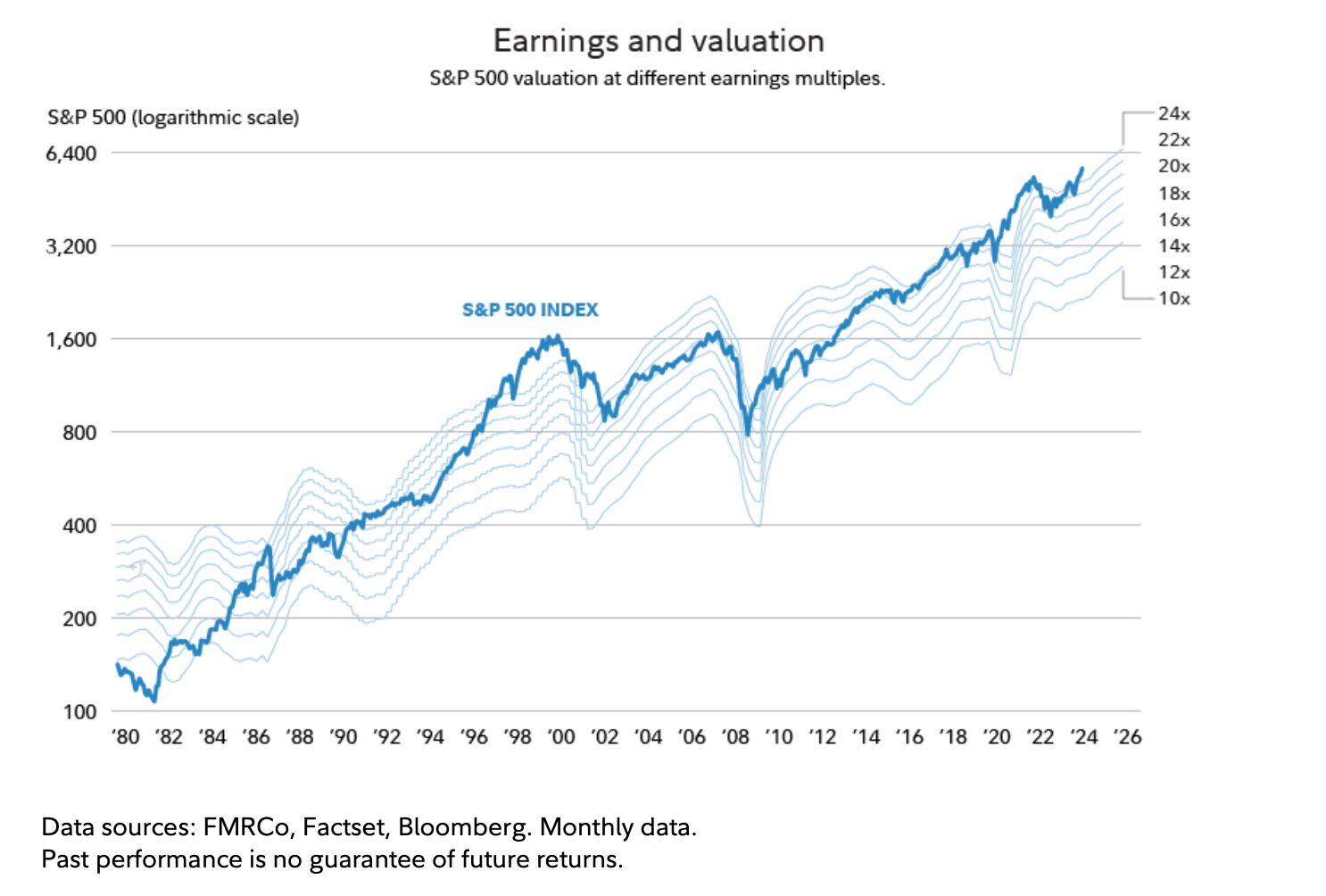

Since the October 2022 low, the S&P 500 has surged by over 40% in total return terms as of mid-March, indicating a relatively youthful phase from a historical standpoint. This youthful nature suggests the potential for an extended duration.

In the realm of secular trends encompassing long-term economic shifts and market cycles, previous cyclical bull markets have yielded maximum returns ranging between 60% to 75%, reminiscent of the 1968 to 1982 period. However, stocks have yet to reach these historical benchmarks in the current cycle. Furthermore, comparisons to the brief 1967–1968 cyclical bull market, which saw a 50% gain, highlight the disparity in gains achieved thus far.

Reflections on the mid/late 1990s cycle prompt consideration of parallels between the current “Magnificent 7” (Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla) and the leading stocks of that era, akin to the “Nifty 50.” Notably, a substantial portion of this cycle’s gains has been concentrated in a select few stocks.

Nevertheless, it’s important to acknowledge the unique nature of each market. Recent months have shown signs of a broadening rally, with less concentration in the Mag 7 compared to much of 2023. Currently, 79% of the market is above its 200-day moving average, indicating increased participation in the rally, even if some stocks are not outperforming the market. This signals a potential shift from the bear market of 2022 to the onset of a new cyclical bull market, with a lot of potential for growth.

This communication is for informational purposes only and is not intended to constitute, and should not be construed as, investment advice, investment recommendations or investment research. You should seek advice from a professional adviser before embarking on any financial planning activity.